Why modernising Papua New Guinea’s bond markets may help solve the foreign exchange shortage

The governor of the Bank of Papua New Guinea, Loi Bakani, says that the shortage of foreign exchange is ‘an issue based on supply and demand of foreign currency for kina.’ One way to increase demand for a nation’s currency is to modernise the bond markets. A World Bank report has looked at some options.

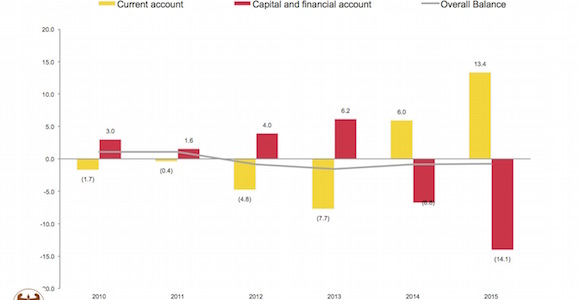

PNG has a current account surplus but financial account deficit Source: Bank of PNG’s Economic Outlook

A possible first step towards creating greater international demand for kina-denominated assets is to create a secondary bond market. This is a marketplace where government (or corporate) bonds are traded, rather than held to until they mature.

At the moment this does not occur in PNG; bonds are held to maturity.

According to an August 2015 World Bank review of PNG’s bond market, the lack of a secondary bond market is a ‘consistent area of concern’ in PNG’s investment community. The report’s observation is not new. As far back as 2011, Nasfund Chief Executive Ian Tarutia was telling Business Advantage PNG that a secondary bond market was ‘long overdue’—comments echoed at the time by the ANZ Bank.

‘PNG’s financial account is in sizeable deficit (the equivalent of 26 per cent of GDP).’

‘Nobody is stopping it happening; it just hasn’t been done,’ one senior financier observes.

Urgency

Yet if the idea is not new, there is now greater urgency.

According to the Bank of PNG’s December 2015 Quarterly Economic Bulletin, the nation has a large trade surplus (the equivalent of 33 per cent of GDP) and a significant current account surplus (the equivalent of 26 per cent of GDP).

Normally, such surpluses would not be associated with a supply-demand problem in a nation’s currency.

But the Bulletin records that PNG’s financial account is in sizeable deficit (the equivalent of 26 per cent of GDP). This is largely attributable to the outflow of foreign currency associated with the end of the construction phase of the PNG LNG project.

‘The current account surplus does not mean high foreign exchange inflows, as mining and petroleum companies were allowed to keep export earnings in offshore accounts to meet overseas liabilities,’ Bakani observed in his recent Economic Outlook for PNG 2016 and Beyond.

Broadening

There are obstacles to making the transition. The World Bank review says developing a secondary bond market and liquidity ‘is a considerable challenge for all emerging markets’.

‘There should also be an effort to ‘broaden the target investor base to develop, promote, and provide access into the local market.’

It says the central bank’s drafting of a Master Repurchase Agreement (MRA) is ‘a positive step in bond market development in that it will by providing market participants and the central bank with liquidity management tools.’

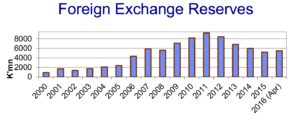

PNG’s foreign exchange reserves Source: Bank of PNG

You also need customers. The review also says there should also be an effort to ‘broaden the target investor base to develop, promote, and provide access into the local market to include: retail customers, corporate entities, insurance companies, small and medium sized enterprises.

‘Registered bidders such as banks and brokers should act as intermediaries and facilitate customers’ primary and secondary transactions.’

Automation

Making trading electronic could be another way to increase demand for, and access to, kina-denominated assets. The review says there should also be an effort to attract non-resident investors into the PNG government securities market by automating the primary market auction system.

‘You just have to copy and paste and put some regulations in place.’

‘The Bloomberg auction system provides a fast and efficient bidding process with a high degree of operational risk mitigation by transitioning from a manual to a highly automated process.’

Privately, many in PNG’s financial community agree. ‘Bloomberg has a fairly decent platform for auctions and they can introduce that tomorrow,’ says one financier.

‘Obviously, you need to have a clearing house and you need to have some regulation around it because you don’t want some international punter wrecking the market.

‘In the low yield world that we live in, 11.5 to 12 per cent on five year paper is very attractive.’

‘But that has been done in various countries over the world. You just have to copy and paste and put some regulations in place.’

Attractive yield

At the moment, bids for PNG bonds are paper-based and have to be lodged in person. The trade is also usually completed by hand, with a cheque.

On the face of it, PNG financial assets have a competitive advantage in the international environment. The yield on PNG bonds should be appealing in global markets currently plagued by low interest rates.

‘In the low yield world that we live in, 11.5 to 12 per cent on five year paper is very attractive,’ observes one industry insider. ‘If you have an electronic auction then an international punter can make a bid and actually participate. Obviously, there are currency risks, and other risks, but 12 per cent is 12 per cent.’