Papua New Guinea government facing ‘difficult’ cash flow challenge says ADB

The Papua New Guinea government faces challenges in managing its cash flow, according to Yurendra Basnett, PNG Country Economist for the Asian Development Bank (ADB). The ADB’s Outlook 2016 paper on the Asian region says PNG’s debt servicing costs are likely to rise.

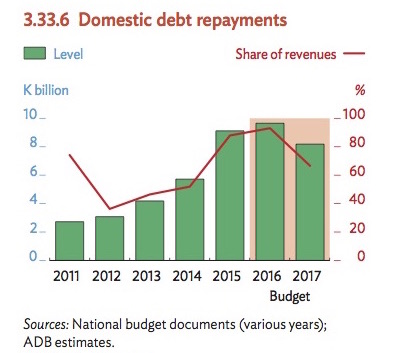

PNG’s domestic debt repayments. Source: ADB Outlook

‘Cash-flow management is growing more difficult for the government as commercial banks reach their technical limits for exposure to government debt,’ the Outlook says. ‘The government is exploring options to float a US$1 billion sovereign bond in 2016 to help refinance current borrowing, but this could prove costly.’

‘As domestic debt has shifted to shorter maturities, interest costs and refinancing risks have risen.’

Basnett says the precise limit for the banks’ exposure to government debt is unknown. ‘It is likely to vary between banks and likely to be linked to their risk appetite and balance sheets. I believe some of the commercial banks may have already reached that limit and are not purchasing new government securities.’

Debt servicing

The ADB’s Outlook says external debt servicing costs appear ‘likely to increase given downward pressure on the kina’. It anticipates that this year the cost of domestic debt servicing will increase significantly. According to the ADB, domestic debt stands at about 28 per cent of GDP, while external debt equals 12 per cent of GDP.

The ADB’s Yurendra Basnett

‘Nearly half of the domestic debt (48.1 per cent) is in Treasury bills for which yields have risen and maturity dates shortened,’ the Outlook says.

‘In 2014, no Treasury bills matured in less than 100 days, but at the start of 2016 such short-term Treasury bills accounted for an estimated 24 per cent of the portfolio outstanding.

‘As domestic debt has shifted to shorter maturities, interest costs and refinancing risks have risen.

‘The 2016 budget estimates domestic debt repayments coming due this year will reach US$3.0 billion, equal to a worrying 93.1 per cent of projected current revenue.’

Short dated debt

Basnett says the shift towards more short dated maturities ‘is driven by risk appetite and liquidity preference of the participants in the public debt market.’ He believes the Government’s debt strategy will need to change.

‘Debt restructuring, through lower interest and longer tenor (length of the loan), will provide short-term relief from the pressures on the public purse to service debt on the books,’ he says.

‘Getting the price of the exchange rate right is part of the issue, but it is equally important to consider the impact of uncertainty.’

‘However, the medium-term solution is to start addressing the underlying drivers of domestic debt by prioritizing expenditure, allocating budget outlays based on performance (things that are going to deliver social and economics results), not using Treasury Bills for large capital items and placing the deficit on a disciplined downward path.’

Positive economic fundamentals

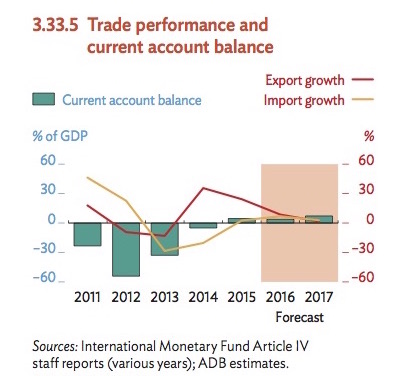

Many of the economic fundamentals in PNG are positive. According to the Bank of Papua New Guinea’s December 2015 Quarterly Economic Bulletin, last year the country recorded a trade surplus and a current account surplus. It was only on the financial account that there was a sizeable deficit.

PNG’s trade and current account balance. Source: ADB Outlook

The Bank’s Bulletin says total non-mining GDP is expected to grow at 3.4 percent this year, up from 2.4 percent in 2015.

This has not alleviated the pressure on the exchange rate, however, and there is a persistent shortage of foreign currency. How can the government deal with the lack of demand for the kina?

Basnett says the problem has several dimensions. ‘Theory tells us that if there is a shortage then there should also be someone willing to trade. So the question ought to be: “Why is that not happening?” Getting the price of the exchange rate right is part of the issue, but it is equally important to consider the impact of uncertainty.

‘Unwinding after a large foreign investment in a context of weak institutions to manage the transition’ was always going to be challenging for PNG.

‘Hence, price adjustment alone might not be sufficient. There is a behavioral component that is being influenced by uncertainty. So those who hold US dollars (the suppliers) seem to be unwilling to trade. If only the price is adjusted there is no guarantee that it will bring certainty, and could result in continued shortage, but at a lower price point.

‘So policies that aid in rediscovering an equilibrium exchange rate, coupled with reforming the exchange rate market, are likely to provide a more durable solution.’

Transition

Basnett adds that ‘unwinding after a large foreign investment in a context of weak institutions to manage the transition’ was always going to be a challenge. The downturn in commodities prices has further accentuated the difficulties, he says.

‘The size of deficit should be controlled and expenditure re-prioritized.’

Basnett argues that although the ‘opportunity cost’ of public expenditure has risen sharply for the Government, he believes it is vital to keep the spending ‘momentum on infrastructure and social outlays’, which he says is ‘imperative for long-term growth.’

‘In the immediate-term, the size of deficit should be controlled and expenditure re-prioritized, and along with it necessary public finance management reform identified by the Government should be implemented without delay. This will directly alleviate the tricky financial issue—public cash flow management.’