MYEFO: Papua New Guinea’s international debt standing and forex still a problem

What the Mid-Year Economic and Fiscal Outlook reveals about Papua New Guinea’s international debt standing and foreign exchange markets.

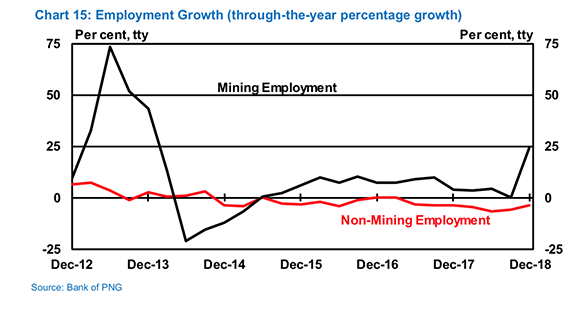

Employment growth data shows that non-mining employment has stagnated in the past seven years but mining employment has recently risen slightly. Credit: Bank of PNG

In the short term, PNG’s foreign exchange difficulties are worsening.

The MYEFO report released by PNG’s Treasury points to a lack of supply of US dollars into the PNG market, due to an ‘unanticipated decline in external borrowing by the Government over the first half of 2019.’

The report says the foreign exchange backlog program has been halted and that ‘the backlog has widened further in recent months.’

Debt

On the positive side, there is the prospect that future debt will be cheaper to serve.

‘Our sovereign bond price is up strongly in secondary trading, meaning the cost to raise funds internationally for us has fallen significantly,’ the MYEFO report says.

‘Lower interest rates internationally have underpinned emerging market sovereign bond issues, with PNG’s sovereign US bond rates declining over 100 basis points (one per cent) since its issuance late last year. This is good news for future issuances.’

The initial interest rate on the sovereign bond was 8.37 per cent. The rate on PNG Treasury bills is currently 6.85 per cent, meaning that the rates on PNG’s domestic and international debt are converging.

After the sovereign bond issue, about 7 per cent of PNG’s government debt is denominated in US dollars, which has allowed the government to diversify away from its dependence on domestic banks and other financial institutions to buy its debt.

‘The performance of the budget over the first half of the year has been difficult. Whilst the 2019 Budget remains a credible document, there was some expenditure towards the end of 2018 that was paid for in 2019 and had to be reversed.’

The secondary market also creates new demand for kina-denominated assets, the absence of which is the main reason for the dearth of foreign exchange.

GDP growth

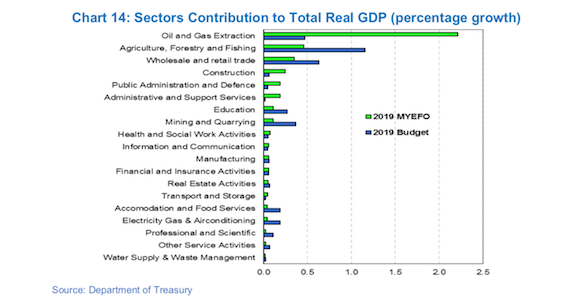

The MYEFO report has a mostly positive outlook for the PNG economy. It projects real (after inflation) GDP growth at 4.4 per cent this year.

It says the domestic economy ‘remains subdued’, but argues ‘with the recovery of the LNG sector to full production in 2019, the oil and gas sector will add strongly to growth.’

The report acknowledges that the government’s finances are under pressure, however.

‘Total public debt stock is expected to increase to K28.126 billion, or 31.8 per cent of GDP.’

‘The performance of the budget over the first half of the year has been difficult. Whilst the 2019 Budget remains a credible document, there was some expenditure towards the end of 2018 that was paid for in 2019 and had to be reversed.

‘This K500 million in expenditure, which covered Services Improvement Programs (SIP) payments, and rental, utility and APEC arrears, was then put into 2019, making execution of the 2019 budget quite problematic.’

The report says 2019 total government revenue and grants are projected to decrease by K257.1 million.

Total expenditure and net lending is projected to increase by K249.3 million which will ‘result in an increase in the fiscal deficit of K506.4 million to K2,373.2 million.’

Total public debt stock is expected to increase to K28.126 billion, or 31.8 per cent of GDP.

The report says that debt levels remain ‘manageable’, however.

Assumptions

The MYEFO report forecasts the price for metals for 2019 to be:

- Gold $US1302 (K4399)/ounce

- Copper US$6070 (K20,495)/ton

- Nickel US$9072 (K30,631)/tonne

These estimates are all close to the 2019 Budget forecasts. The cobalt price, however, is forecast to fall sharply in MYEFO. It is predicted to be US$22,606 (K76,3290/tonne in 2019, compared with the 2019 Budget forecast of US$46,682 (K15,762)/tonne and the 2018 actual price of US$72,819 (K245,873)/tonne.

[infogram id=”myefo-1ho16vdnqw0q6nq?live”]